With all the uncertainty lately about the Coronavirus, it is understandable that you may be asking what’s next. Will events like the Coronavirus have an impact on you being able to reach your personal and financial goals? Money isn’t the most important thing in life, but it does help you to accomplish some goals. Part of the burden is trying to sort through the news cycle to determine 1) what applies to your situation and 2) what you can control. My aim in this article is to help you to better understand both the current market environment and the threat the Coronavirus could pose to your portfolio. But keep in mind that this is no substitute for actually sitting down, identifying your goals, and developing a plan to achieve them! Financial planning should inform your investment decisions, not the other way around.

Market Sentiment

Investor Optimism

Monday, January 27th, was an important day in the market. It marked the end of a remarkable streak of calm in the S&P 500. The loss ended one of the S&P’s longest ever streaks-73 days- without a daily change of more than 1% in either direction.

It also marked the end of the 30 session streak, where the S&P 500 had not had back-to-back losses.

I mention these two statistics because I believe it is essential to understand the greater context of the market environment in which you are investing. As of late, investor optimism has reached the point of extreme bullishness. Historically, this is a bearish signal, at least in the short-term, for the overall stock market.

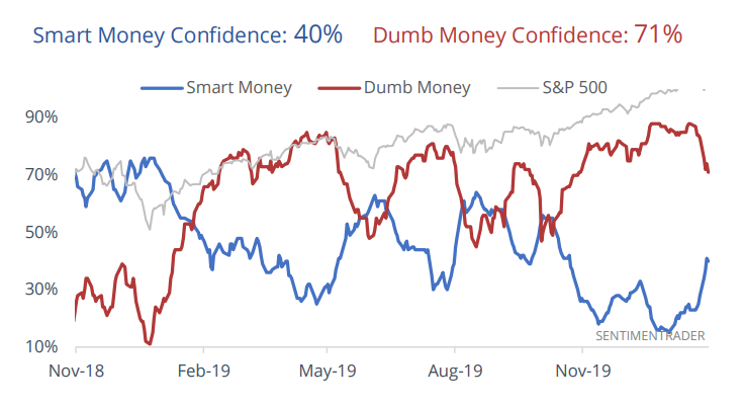

Smart vs. Dumb Money

One of my favorite investor sentiment indicators is the Smart Money and Dumb Money Confidence Index.

It shows what two different groups of investors are doing. The “smart” money is large commercial hedgers, institutional traders, or speculators. The “dumb” money is the smaller odd-lot traders or speculators. Two weeks ago, we were at one of the most extreme sentiment windows in 20 years. It was something quite out of the ordinary.

When things become this stretched, we typically will experience a reversion to the mean in optimism and market returns. But there always must be a catalyst. I believe there is a reasonable chance that we may have just experienced it.

The Catalyst

Wuhan and Corona

In mid-January, major news outlets began to report about the spread of a disease of the coronavirus family of viruses in Wuhan City, China. The first case of Coronavirus (2019-nCov) was first reported to the WHO (World Health Organization) on December 31st.

Is It Comparable to SARS?

The news media has made comparisons to the Severe Acute Respiratory Syndrome (SARS), another virus in the corona family that appeared in China in 2002.

SARS infected 8,096 people over 9 months from 2002 to 2003. Over the last month, almost 20,000 individuals have been diagnosed with the Coronavirus. That is a dramatic difference, but it is critical to remember that SARS had a fatality rate of 9.5% compared to the current fatality rate of 2.2%.

One of the most significant differences between now and then is that in 2003 only 6% of the Chinese population had access to the internet. That number has increased tenfold to more than 61%. The hope is that awareness will help to slow the further transmission of the virus.

3 Ways the Coronavirus Could Impact the Market

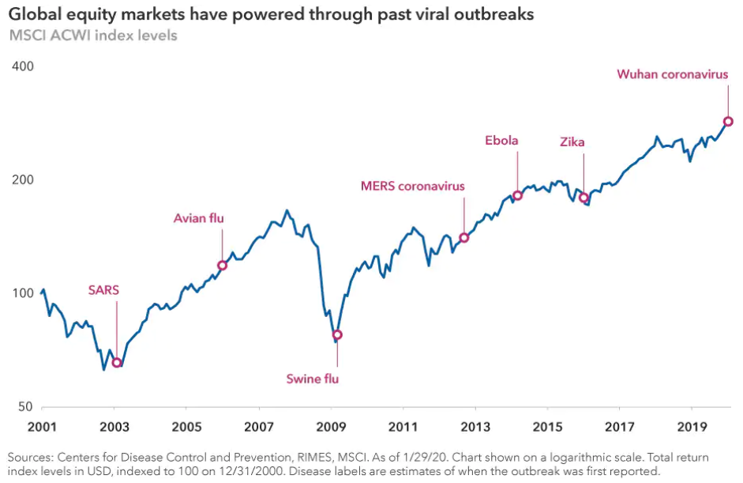

Based on the numbers coming out of the Chinese government, many economists and financial institutions believe that the U.S. economy is strong enough to weather any economic impact related to the Coronavirus. Any economic impact will only be temporary. They point to prior past viral outbreaks.

Although the market could be looking past the economic impact of the Coronavirus, there are a few things that could cause the market to reassess this assumption.

China’s Economic Growth

Even before the first case of Coronavirus in Wuhan, China’s economy was already growing at the slowest rate in 30 years.

Over the last decade, China has seen its travel and tourism activity skyrocket. The transition of China’s economy to one that is more services-based could prove to be problematic for economic growth in the short-term. The Chinese government has issued quarantines for Wuhan and 15 surrounding cities, which represent more than 50 million people. The quarantine is occurring during the middle of the Chinese Lunar New Year. This year, the number of trips made in China over the Lunar New Year break has fallen by 73% from last year.

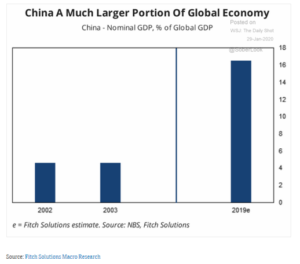

It wasn’t surprising that the People’s Bank of China announced that they would inject $21.7B worth of liquidity into markets, when the Chinese markets reopened, to help cushion the impact of the Coronavirus. Global markets welcomed this news as Chinese GDP now represents more than 16% of the global economy. China is playing a more critical role in the world’s economy.

Supply Chain Disruption

As you may have seen it reported in the news, many U.S.-based airlines are canceling flights to China. Several companies, such as Starbucks, Disney, and Apple, have closed their retail stores and corporate offices through February 9th.

There are growing concerns about supply-chain disruptions. Per the latest Organization for Economic Cooperation Development (OECD) reports, China is the world’s largest exporter of intermediate products at 20%.

In layman’s terms, many factories are reliant on inputs that come from China. The longer the Coronavirus curtail’s China’s industrial output, the bigger the risk other countries output is disrupted as well.

The Trade War

Before the ink had dried on the trade agreement, there were questions about China’s ability to buy $200B of goods from the United States over the next couple of years. Given the impact of the Coronavirus, the hope is that China will be able to make good on their purchase in the second half of 2020.

There is now talk that Chinese officials may be hoping for some flexibility on their pledges. Market watchers are turning their focus to one specific line in the trade deal. It reads that “in the event that a natural disaster or other unforeseeable event” delays either party from complying with the agreement, the nations will consult. The question remains. If the Chinese don’t meet the terms of the agreement are the tariffs back on?

Learn the 7 Things You Need To Know About Market Corrections

Eyes on the Ball, A Hand on Your Wallet

The shell game is a game that employs a confidence trick to perpetrate a fraud. Before the Coronavirus, U.S. markets had been able to shake-off any economic uncertainties (trade wars, inverted yield curves, and impeachment proceedings). It would be easy to assume that this would be the case once again.

However, the Coronavirus poses a multi-faceted problem. Its impact is both domestic and international. It concurrently impacts both supply and demand. At the same time, it could influence manufacturing along with service sectors. Currently, there isn’t a way to know the effects of the Coronavirus as it works its way through the system. Or even how long it might take to do so. But those who dismiss the potential impact of the Coronavirus are assuming that any problems are temporary, containable, and reversible. It may be presumptive to think those questions can be answered right now.

Time To Panic?

This article led with the information regarding investment sentiment for a reason. There are many different cycles when it comes to markets and investing. It is vital that you properly understand where we are at in the cycle(s). If you are unaware of the environment, you run the risk of being distracted by the daily news headlines. Perhaps, even led to panic.

As we have mentioned for the past several months, presidential election years typically have more volatility in the first half of the year. Election year rallies have a common variable. They occur only after the market has identified the likely winner—regardless of the political party.

We also ended the month of January with extreme levels of investor optimism. Given how these two cycles are juxtaposed, it should not be surprising to see a healthy market pullback of 5-10%. As we mentioned in our last Market Update, trees can’t grow to the sky. Periodically, investors’ return expectations and risk levels need to be reset. More often than not, a market pullback will accomplish this.

What to Do?

If nothing else was learned from the market decline in 2018 and subsequent rebound, at least let it be this one thing: timing the market is impossible.

As we were saying back in December of 2018 when the market was down almost 20%, it is critical that you understand 1) your tolerance for risk and 2) how much risk is in your portfolio. If this sounds like a broken record, then good. We are succeeding in our job!

By taking these two steps, investors are better able to set their expectations for investment returns and volatility going forward. Remember, reactions in the short-term make bad long-term retirement decisions. Most investors are best served by taking the appropriate level of risk and weathering temporary fluctuations in the markets.

Click here to learn more about how Hedgefield Wealth Management can help to remove the burden of managing your wealth.

Hedgefield Wealth Management is a registered investment adviser. Hedgefield Wealth Management does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Sources:

https://www.thecapitalideas.com/articles/china-economic-slowdown

https://qz.com/1790719/china-coronavirus-outbreak-unfolds-in-a-new-age-of-information/

https://www.worldometers.info/coronavirus/coronavirus-death-rate/

{kind=link}